Introduction

When a spouse gambles away savings, loses money on reckless investments, or drains accounts after separation, can the other party ask the court to add it back to the property pool? This mechanism is called an add-back.

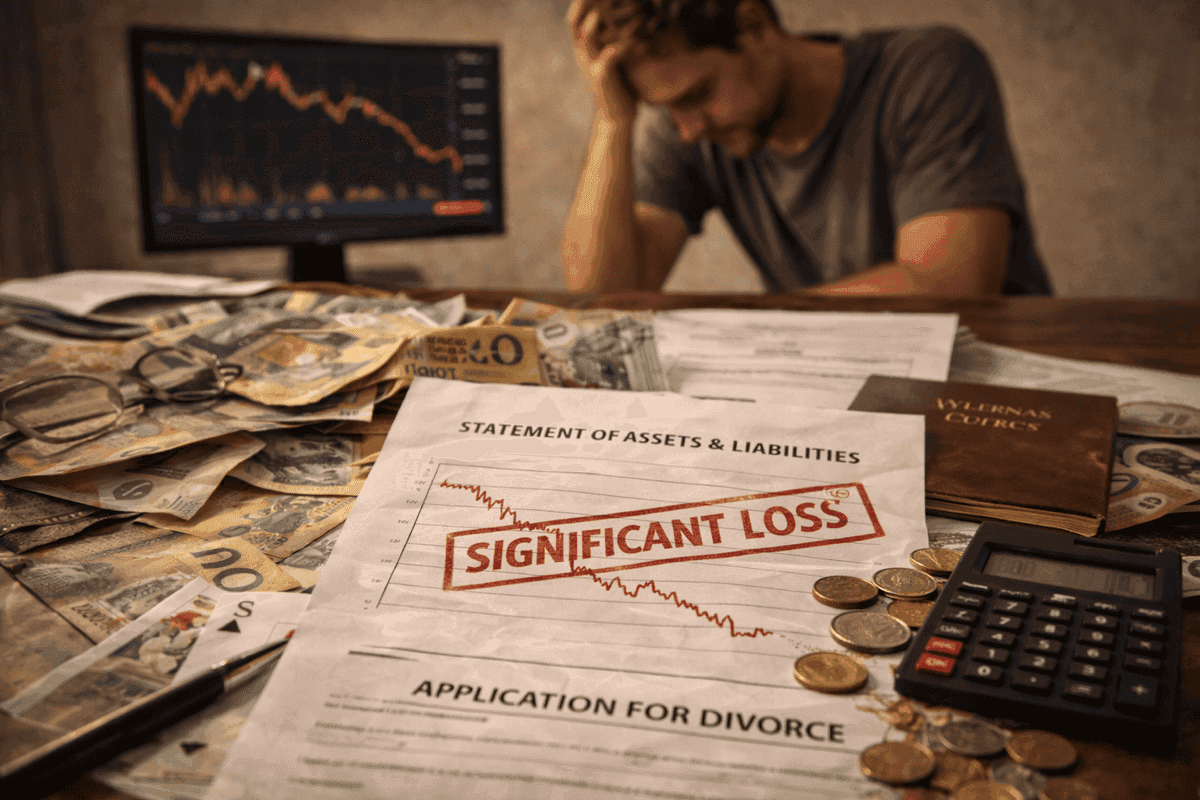

Q1: Can I recover money my spouse gambled away?

A: Gambling losses can be recovered if the spending was grossly out of proportion to family income. In James, the husband withdrew over $80,000 at gaming venues over nearly three years on a family income of just $100,000 per year. The court found this was waste and ordered a 5% adjustment in the wife's favor. Reference: James & James [2013] FCCA 1188

Q2: Do investment losses count as waste?

A: Most investment losses are not recoverable. The court treats market-driven losses as part of life, not waste. In Idoni, a financial professional lost over $500,000 in the GFC. The court held this was a risk nobody could have predicted and made no add-back. But if someone ignores fraud warnings and keeps investing, that crosses into reckless conduct. Reference: Idoni & Idoni [2013] FamCA 874

Q3: What if my spouse spends everything after we separate?

A: The court can count post-separation spending against the spender's share. In Rockman, the husband spent his entire $122,000 super after separation, claiming living expenses. Evidence showed he lived in the family home and gambled at casinos. The court treated this as a premature distribution and ordered an 8% adjustment in the wife's favor. Reference: Rockman & Rockman [2014] FCCA 1966

What Counts as Reckless or Wanton Conduct in Asset Wastage Claims?

The foundational rule was set in Kowaliw & Kowaliw [1981] FamCA 70: losses are generally shared between both parties unless they were incurred recklessly, negligently or wantonly.

The husband spent $43,390 on pornography, prostitutes, and sugar daddy websites during the relationship. The wife argued this should be added back to the property pool.

The husband said the spending was a personal choice during the relationship and should not affect the property division.

Outcome: The Court found the expenditure was reckless, negligent or wanton and ordered the full amount notionally added back to the property pool.

"The expenditure bears the characteristic of being reckless, negligent or wanton, the overall effect of which was to reduce or minimise the pool of assets... it cannot be a just and equitable order from the wife's perspective if the sum in question is arbitrarily excluded from the pool of assets available for distribution between them."

It does not matter how much you earn. If you blow part of it on something reckless, the court will not write it off. The court looks at why the money was spent. If the spending only served one party's wanton desires and shrank the shared pool, the other party can recover it through an add-back.

When Does an Investment Loss Become Reckless Rather Than a Market Risk?

Many people confuse a bad investment with a reckless one. The court draws a line between losses that are just part of life (vicissitudes of life) and losses caused by deliberately ignoring financial safety.

The wife, aged 86, lost $360,000 to fraudulent overseas brokers. Her financial planner told her to pick safe options. Her bank sent suspicious dealing alerts. A Fraud Refund label even appeared on her account. She kept sending money. She argued her age and possible depression made her vulnerable.

Outcome: The Court found her conduct was reckless and wanton. Despite her age, the repeated warnings she received and ignored showed she had the information to avoid the loss. The $360,000 was notionally added back to the property pool.

In contrast, in Idoni & Idoni [2013] FamCA 874, a financial professional lost over $500,000 in highly geared blue chip shares just before the GFC.

Case Comparison: Reckless Waste vs. Commercial Risk

| Feature | Anaya & Anaya [2019] | Idoni & Idoni [2013] |

|---|---|---|

| Type of Loss | Fraudulent Investment Scheme | GFC-related Share Market Crash |

| Prior Warning | Received bank alerts and fraud labels | None (unforeseeable economic event) |

| Professional Status | Not a professional investor | Qualified financial professional |

| Court's Finding | Reckless and Wanton Conduct | Ordinary Commercial Risk |

| Outcome | $360,000 notionally added back to pool | No add-back or adjustment for share loss |

"Neither the husband nor the broader community could have reasonably foreseen the scope of the global financial crisis... the share trading losses, whilst unfortunate, were simply the vicissitudes of life."

If the loss was something nobody could have predicted, like a global financial crisis, the court will not penalise you for it. But if you ignored clear warnings and kept throwing money in, that is reckless.

The Idoni ruling protects people from being penalised for genuine commercial failures. However, if a professional sits back after separation and watches a super fund get destroyed, the court may still adjust the split. In Idoni, the husband stood mute while a super fund was decimated. The court applied a percentage adjustment under section 75(2)(r) of the Family Law Act for poor management.

When Does Gambling or Lifestyle Spending Become Legally Recoverable Waste?

Gambling and alcohol are often cited as grounds for wastage. But simply proving your spouse gambled is not enough. You need to show the spending was excessive relative to the family's income.

Over nearly three years, the wife identified $83,798 in withdrawals from the joint account, mostly at hotels with gaming facilities. The family earned about $100,000 a year.

The husband did not dispute the withdrawals but said his gambling was recreational.

Outcome: The Court found the husband's gambling and associated spending on alcohol and food was waste and ordered a 5% adjustment in the wife's favour. In small property pools, the court may prefer a percentage adjustment rather than a strict dollar-for-dollar add-back.

"I am satisfied that the husband's gambling and associated expenditure on alcohol and food is waste and that there should be a 5% adjustment for this consideration."

The court measures your gambling against what the family earns. When you blow a huge chunk of household income at gaming venues, the court steps in to protect the other party.

In Rockman & Rockman [2014] FCCA 1966, the husband spent his entire pre-separation super ($122,555) after separation. He claimed it was for living expenses, but evidence showed he lived in the family home and gambled at a casino.

"He has therefore made a premature distribution of what would otherwise have been matrimonial property... accordingly there will be an adjustment in the wife's favour of 8%."

There is a difference between genuinely needing money to live and grabbing assets for yourself after separation. If you spend down a joint asset with no good reason, the court treats it as if the money is still there and counts it against your share.

Can Legal Fees and Insurance Payouts Be Added Back to the Property Pool?

Many people assume money spent on lawyers is gone for good. The court often sees it differently. Paying your lawyer from joint funds is a premature distribution.

In Idoni & Idoni [2013] FamCA 874, the husband drew $25,000 for legal fees from joint funds. The court made a specific adjustment of $12,500 in the wife's favour to even things out.

In Anaya & Anaya [2019] FCCA 1048, the court even added back life insurance payouts sent to the husband's estate. The policies were owned by the husband before the marriage, but the premiums had been paid from joint resources for 45 years.

"The policies clearly formed part of the parties' assets which the husband had a duty to preserve... I am satisfied that the funds paid under the policies should be notionally added back to the property pool."

You have a duty to preserve shared assets. Whether it is a life insurance payout or a super balance, you cannot funnel marital wealth to someone else and expect the court to ignore it.

What Should You Do If You Suspect Asset Wastage?

The cases above reveal the core principles courts apply in asset wastage disputes:

The nature of spending matters more than the amount. Sattle & Easton established that even if the amount is a small fraction of total income, spending that is reckless, negligent or wanton will be fully added back. The key question is not how much was spent, but why.

Ignoring warnings is reckless. Anaya & Anaya set an important benchmark: if you receive clear fraud warnings and ignore them, the court will find reckless conduct regardless of your age or vulnerability.

Gambling is measured against family income. James & James shows that the court looks at gambling in proportion to what the family earns. When spending is grossly out of line with household income, percentage adjustments protect the other party.

Do:

- Keep bank statements and withdrawal records as evidence

- Work out the exact dollar amount and whether it fits an add-back or a percentage adjustment

- Figure out if the spending was just life happening or genuinely reckless

- Lock down joint assets as soon as you separate

Don't:

- Accuse your spouse of wasting money without paperwork to back it up

- Walk into court saying they wasted heaps without specifics

- Call a normal business loss wastage

- Sit back while your spouse drains shared accounts and only act later